Europe’s Digital Ad Market: Growth Is Moving Toward Video, Retail Media and Automation

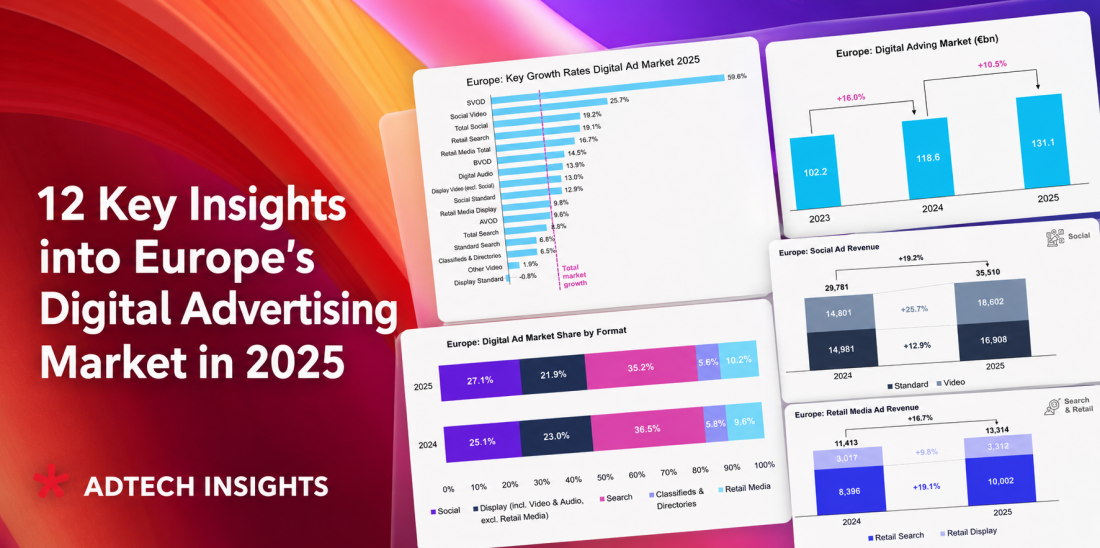

Europe’s digital advertising market continued to grow in 2025, but the most important story is not just the size of that growth. According to IAB Europe’s AdEx Benchmark 2025 Report, the market reached €131.1 billion, growing 10.5% year over year, yet the dynamics behind this expansion show a clear structural shift. Growth is moving away from generic digital inventory and toward environments that offer stronger attention, richer data, commerce intent and better automation. We’ve selected 12 key insights that defined digital ad market developments and key trends in advertising budget allocation over the past year.

- 1. Growth continued, but normalized after the 2024 rebound

- 2. Digital advertising is outperforming traditional media more strongly

- 3. The ad market remains highly concentrated, but growth comes from less mature regions

- 4. The format mix is shifting away from standard display and classic search

- 5. Video is the central growth engine of the ad market

- 6. Social growth is now clearly video-led

- 7. Retail media became a structural category, not a niche

- 8. Search is still the largest category, but its growth is increasingly retail-driven

- 9. Standard display is under pressure

- 10. Programmatic growth is also video-led

- 11. Audio is smaller, but growing above market rate

- 12. AI is already affecting supply-side economics

- Main conclusion for European Ad Market Development in 2026

1. Growth continued, but normalized after the 2024 rebound

The European digital ad market reached €131.1 bn in 2025, adding €12.5 bn year over year. Growth slowed from +16.0% in 2024 to +10.5% in 2025, so the market is still expanding strongly, but at a more normalized pace. Inflation-adjusted growth is lower at +9.4%, mainly because Turkey and Ukraine inflated the nominal growth number.

Insight: the market is no longer in post-pandemic rebound mode. Growth is becoming more structural and selective.

2. Digital advertising is outperforming traditional media more strongly

The report shows that digital’s outperformance versus traditional media increased to 17.0 percentage points in 2025, up from 13.7 pp in 2024. IAB links this to advertiser migration to digital, AI-driven automation, and the continued shift to digital video across both social and non-social environments.

Insight: digital ad growth is not only following the macro cycle. It is taking over more functions from the broader media, commerce and sales infrastructure.

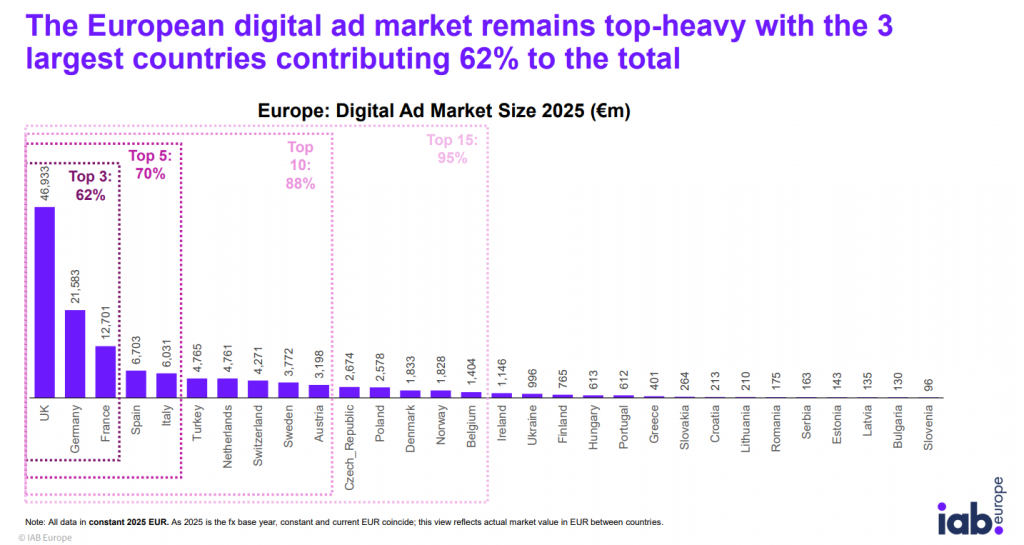

3. The ad market remains highly concentrated, but growth comes from less mature regions

Europe’s digital ad market is still top-heavy: the UK, Germany and France account for 62% of total market value, while the top 10 markets account for 88%. At the same time, all 30 markets grew, 16 posted double-digit growth, and the 10 fastest-growing markets were all in Central and South-Eastern Europe.

Insight: market value is concentrated in mature Western European markets, but the highest growth momentum is coming from less mature CEE and SEE markets.

4. The format mix is shifting away from standard display and classic search

The market share of Social increased from 25.1% to 27.1%, while Retail Media rose from 9.6% to 10.2%. By contrast, Search declined from 36.5% to 35.2%, and non-social Display fell from 23.0% to 21.9%.

Insight: growth is not evenly distributed across digital. Budgets are moving toward formats with stronger attention, commerce intent, automation and measurable outcomes.

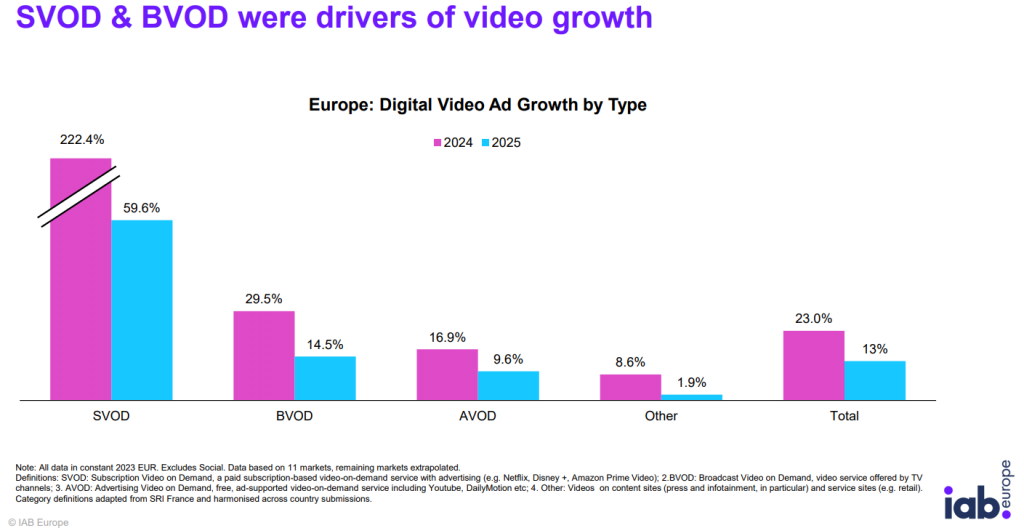

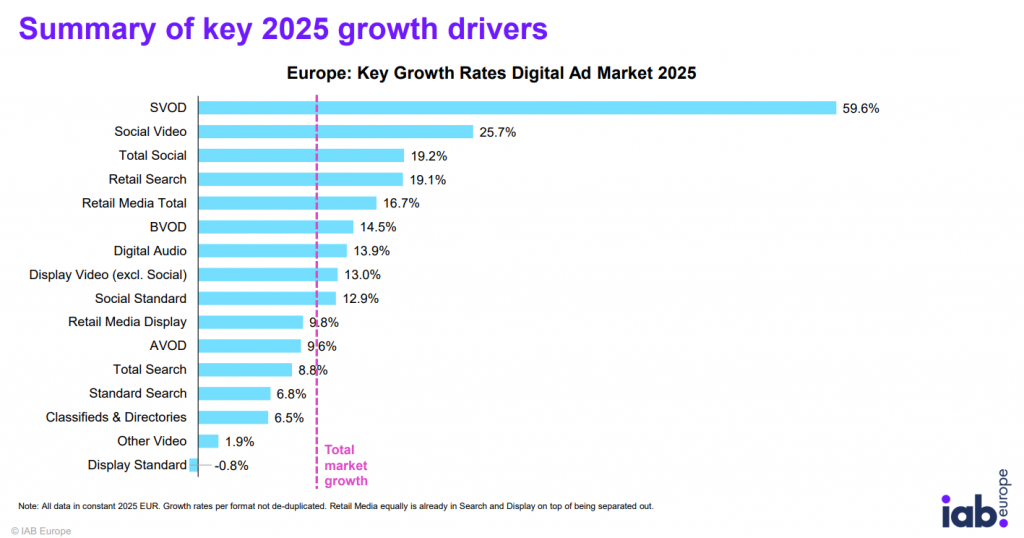

5. Video is the central growth engine of the ad market

Total video advertising grew by 19.6% to approximately €34.0 bn. For the first time, video accounts for more than half of display investment in Europe. Social video grew 25.7%, while display video excluding social grew 13.0%. The highest growth format in the entire report was SVOD, up 59.6%.

Insight: video is no longer just a sub-format. It is becoming the main growth layer across social, display, streaming and programmatic buying.

6. Social growth is now clearly video-led

Social advertising grew 19.2% to €35.5 bn. Within that, social video grew 25.7% and now represents 52% of total social ad revenue. Standard social still grew, but at a lower rate of 12.9%.

Insight: social platforms are increasingly capturing budgets through video-first formats rather than standard feed or static placements.

7. Retail media became a structural category, not a niche

Retail Media grew 16.7% to €13.3 bn, passing 10% of total European digital ad spend for the first time. Retail Search was the main driver, growing 19.1%, while Retail Media Display grew 9.8%.

Insight: retail media is becoming a core part of digital advertising infrastructure, especially because it connects media spend with commerce data, purchase intent and sales measurement.

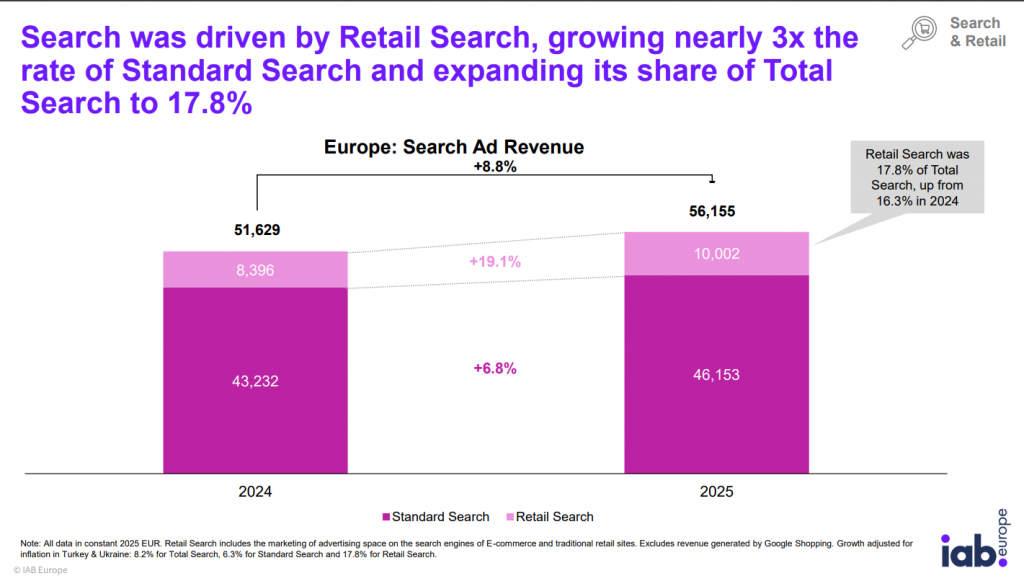

8. Search is still the largest category, but its growth is increasingly retail-driven

Total Search grew 8.8% to €56.2 bn, but Standard Search grew only 6.8%. Retail Search grew 19.1%, nearly three times the rate of Standard Search, and increased its share of Total Search from 16.3% in 2024 to 17.8% in 2025.

Insight: search budgets are gradually fragmenting. Growth is moving from classic search engines toward commerce and retail search environments.

9. Standard display is under pressure

Non-video standard display declined by -0.8%, while display video grew 13.0% and digital audio grew 13.9%. This is one of the clearest signals in the report: static display formats are losing momentum unless they are connected to video, richer creative, data or programmatic activation.

Insight: generic display is becoming a weak growth format. The future of display is more video-led, data-led and automated.

10. Programmatic growth is also video-led

Programmatic ad spend excluding social grew 10.9% to €15.8 bn, faster than total display growth of 5.9%. But within programmatic, video grew 19.8%, while programmatic display declined -1.2%.

Insight: programmatic is still expanding, but its growth engine is no longer standard display. Programmatic growth is shifting toward video inventory.

11. Audio is smaller, but growing above market rate

Digital Audio reached €1.23 bn, growing 13.9%. Podcasts grew 16.7%, while other audio formats, including music streaming and internet radio, grew 11.8%.

Insight: audio is not yet a dominant budget category, but it is becoming a meaningful incremental channel, especially as advertisers look for addressable, attention-based environments beyond display and search.

12. AI is already affecting supply-side economics

The report frames AI’s first-order 2025 effect as supply-side: cheaper creative production, better optimization, more automation and productivity gains, especially for smaller advertisers. It also notes that second-order effects on search behavior, agentic buying and budget allocation are only beginning to appear.

Insight: AI is not yet shown as a separate ad-spend category, but it is already changing the cost structure, buying efficiency and competitive dynamics of digital advertising.

Main conclusion for European Ad Market Development in 2026

The European digital advertising market in 2026 is growing through three main forces:

- Attention shift – video, social video, SVOD/BVOD and audio are capturing more budget.

- Commerce shift – retail media and retail search are taking share from classic search and performance channels.

- Automation shift – programmatic and AI-enabled optimization are reshaping how budgets are planned, activated and measured.

The clearest strategic takeaway: growth is moving away from generic digital inventory and toward channels that combine attention, data, commerce intent and measurable outcomes.

Looking for comprehensive monetization of commercial or retail media? Try Retail Media Machine ad platform for managing ads across onsite, offsite, and in-store resources.

Contact us for more information and demo.